Private Hospital Facts

The Australian Private Hospitals Association (APHA) compiles PH Facts based on annual data. It is updated as authoritative facts, figures, trends and research about private hospital activity and the issues facing the sector are published, citing fully attributed data from independent sources.

It is designed as a fast reference to national and state-by-state information about Australia's private hospitals. The APHA has commissioned new research to provide a more comprehensive picture, expected in the second half of 2026. Scan key categories about private hospitals via the section titles in the menu (right of this page) or by scrolling below.

Scope of Activity

Private hospitals in Australia are fundamental to overall health care delivery, with the complementary nature of the public and private hospitals systems negating the polar extremes of the dysfunctional NHS in the UK and private insurance dominated US system. It is why the Australian hospital system has been considered the best in the world...

In 2026 there are 637 private hospitals in Australia, including day surgeries. This is down from the 647 in 2020. While the overall figure points to a decline of 10, in reality some 80 hospitals have closed over that time.

Of the 637 hospitals open today, just 559 were open in 2020. The trend has been for day surgeries, usually doctor owned, to open, so there has been a significant shift in the make-up of the sector.

- - Comparing Private hospital second-tier category list, Department of Health and Ageing, August 2020; and the List of declared hospitals, Department of Health, Disability and Ageing, at July 2025.

In 2023-24 private hospitals in Australia admitted 5,142,645 patients - an increase of 3% on the previous year. Private hospitals account for 41% of all hospital admissions in Australia.

Overnight stays increased by 22,258 to 1,330,167 admissions, while same day admissions increased by 126,610 to 3,812,478.

Increases were experienced across all states (noting data from Tasmania, the ACT and NT is not available).

- - Admitted Patient Care 2023-24, Section 2, How much activity was there?, Australian Institute of Health and Welfare, May 2025.

The following table shows private hospital and public hospital admissions on a state-by-state basis from 2019-20 through to 2023-24. Over the last 12 months, private hospitals accounted for the following percentage of total admissions in each jurisdiction:

- New South Wales - 44.2%

- Victoria - 36%

- Queensland - 42%

- Western Australia - 44.2%

- South Australia - 43.2%

(Note: data is not available for Tasmania, the ACT and NT).

- - Admitted Patient Care 2023-24, Section 2, How much activity was there?, Australian Institute of Health and Welfare, May 2025.

Total patient days increased from 10,415,109 to 10,594,195 - an increase of 179,086. This trend was observed across all states (noting no data is available for Tasmania, the ACT and NT).

- - Admitted Patient Care 2023-24, Section 2, How much activity was there?, Australian Institute of Health and Welfare, May 2025.

In the 12 months to 2023-24, there were 3,812,478 same day admissions in private hospitals (an increase of 3.4% on the previous year), with 1,330,167 overnight admissions in the same period (an increase of 1.7%).

Same day separations as a percentage of the total admissions for private hospitals amount to 74.1%.

- - Admitted Patient Care 2023-24, Section 2, How much activity was there?, Australian Institute of Health and Welfare, May 2025.

Elective surgery admissions in private hospitals increased to 4,113,025 (up from 3,996,254) in 2023-24, while emergency admissions in private hospitals rose to 247,909 (up from 243,932 on the previous year).

- - Admitted Patient Care 2023-24, Section 4, Why did people receive care?, Australian Institute of Health and Welfare, May 2025.

Of the Emergency Department admissions in private hospitals over 2023-24, they were funded as follows:

- 43,328 - via private health insurance.

- 993 - public patients.

- 1,032 - self-funded.

- 1,322 - funded by the Department of Veterans' Affairs.

As a side note: Private health insurance funded 54,412 Emergency Department admissions in public hospitals.

- - Admitted Patient Care 2023-24, Section 6, What procedures were performed?, Australian Institute of Health and Welfare, May 2025.

Across the total admissions to private hospitals over 2023-24, they were funded as follows:

- 4,203,282 - via private health insurance.

- 309,157 - were public patients funded by the states/territories.

- 362,389 - self-funded.

- 133,441 - funded by the Department of Veterans' Affairs.

- - Admitted Patient Care 2023-24, Section 4, Why did people receive care?, Australian Institute of Health and Welfare, May 2025.

Over 2023-24 there were 3,312,121 acute same day admissions and 1,192,256 acute overnight admissions in Australian private hospitals - an overall increase of 112,755.

- - Admitted Patient Care 2023-24, Section 4, Why did people receive care?, Australian Institute of Health and Welfare, May 2025.

Surgical

Private hospitals account for a staggering 70% of all planned surgery in Australia - 1.72 million operations a year. Not only providing the latest procedures and technologies to private patients in state-of-the-art facilities, but taking massive pressure off the public hospital system...

Private hospitals perform most of many of the life-saving and life-changing procedures Australians need throughout their lives:

- 95% - Obesity and Overweight

- 77% - Skin Grafts

- 76% - Coronary Procedures

- 75% - Knee Replacements

- 74% - Hip Replacements

- 72% - Eye Disorders

- 69% - Malignant Skin Cancers

- 66% - Carpal Tunnel Syndrome

- 65% - Spinal Disorders

- 63% - Hernias

- 53% - Malignant Breast Cancers

- - AR-DRG - Operating Room and Major Diagnostic Category 2023-24, Australian Institute of Health and Welfare, 2025.

In 2023-24 private hospitals performed 1,827,599 surgeries, including 48,344 via Emergency Department admissions.

- - Admitted Patient Care 2023-24, Section 6, What procedures were performed?, Australian Institute of Health and Welfare, May 2025.

Of the elective admissions involving surgery in private hospitals over 2023-24, they were funded as follows:

- 1,371,056 - via Private health insurance.

- 59,718 - public patients.

- 131 - self-funded

- 32,415 - funded by the Department of Veterans' Affairs.

- - Admitted Patient Care 2023-24, Section 6, What procedures were performed?, Australian Institute of Health and Welfare, May 2025.

Medical

Often forgotten, private hospitals perform 1.67 million medical treatments every year, often involving interventions Australians need every day...

Private hospitals are major providers of critical medial treatments, often including interventions relied on by Australians every day:

- 69% - Spinal Disorders (non-surgical)

- 66% - Sleep Apnea

- 61% - Female Reproductive Disorders

- 60% - Male Reproductive Disorders

- 54% - Chemotherapy

- 53% - Ear, Nose and Throat Diseases

- - AR-DRG - Major Diagnostic (Medical) Category 2023-24, Australian Institute of Health and Welfare, 2025.

Private hospitals treated 1,666,305 patients for medical conditions in 2023-24, continuing a steady rise since 2019-20.

- - Admitted Patient Care 2023-24, Section 5, What services were provided?, Australian Institute of Health and Welfare, May 2025.

Mental Health

Australia's private acute psychiatric hospitals provide services for patients suffering from moderate-to-severe mental health issues. They complement the public psychiatry hospital system, which treats a different caseload mix - meaning they are not interchangeable, nor do community clinics and out-patient services meet the same acute needs...

Over 2023-24 private acute psychiatric hospitals accounted for 61% of all acute mental health admissions - a decline of 1% to 217,047 (down from 217,851 the previous year).

- - Admitted Patient Care 2023-24, Section 4, Why did people receive care?, Australian Institute of Health and Welfare, May 2025.

Across the mental health admissions in private hospitals for 2023-24, total separations encompassed:

- 1,084,846 - patient days, with an average length of stay being five days.

- 167,483 - specialised psychiatric care days.

- 179,933 - total admissions funded by private health insurance (83%).

- - Admitted Patient Care 2023-24, Section 5, What services were provided?, Australian Institute of Health and Welfare, May 2025.

Rehabilitation

Australia's private rehabilitation hospitals cover a wide array of needs, including recovery from traumatic physical and brain injuries...

There are 35 designated rehabilitation private hospitals in Australia*. Within the APHA membership, there are 54 hospitals providing various levels of rehabilitation services**.

- - *Deptartment of Health, Disability and Ageing, List of declared hospitals, July 2025;

- **Australian Private Hospitals Association, Membership Data, July 2025.

81.5% of all admissions for rehabilitation hospitalisations in Australia are in private hospitals. In 2023-24 admission rose by 36,958 to 396,676 total admissions.

- - Admitted Patient Care 2023-24, Section 4, Why did people receive care?, Australian Institute of Health and Welfare, May 2025.

Of the total admissions in private rehabilitation hospitals in Australia, they were funded as follows:

- 361,090 - via private health insurance.

- 5,003 - were public patients funded by states/territories.

- 3,195 - self-funded.

- 13,414 - funded by the Department of Veterans' Affairs.

- - Admitted Patient Care 2023-24, Section 5, What services were provided?, Australian Institute of Health and Welfare, May 2025.

Maternity

Despite mothers-to-be showing an overwhelming preference for private hospital deliveries - encompassing a full suite of care throughout pregnancy, birth and puerperium - the proportion of private births is plummeting...

Over the decade to 2023-24, the proportion of births in private hospitals has fallen from 30% of total births to just 20%.

In the last year total births in private hospitals fell to 61,618 (down from 64,200 in the previous year).

- - Births, Australia, Australian Bureau of Statistics, 2025.

Australia is experiencing an historic fall in births. There were 286,998 births registered in 2023, with declines across all states and territories. There has been an 5.68% fall (a drop of 17,270 births) in birth rates since 2015-16.

- - Comparing data from Australia's mothers and babies 2015, Australian Institute of Health and Welfare, (released 2017); with Births in Australia, Australian Institute of Family Studies, December 2024.

In a recent research article, published in the Medical Journal of Australia, a study found that:

"Our preliminary modelling is predicting that the number of births occurring in Australian private maternity hospitals are likely to fall precipitously. So quickly that, by the end of the decade, private maternity hospital will cease to exist."

- - See MJA article at: Private maternity hospitals: extinct by the end of this decade?, July 2024.

Over the last decade, 14 private hospital maternity wards have closed (including two hospitals which closed entirely).

- - See story at: Why HealthScope maternity closures are an 'absolute crisis' and a symptom of a bigger problem, Australian Broadcasting Corporation, February 2025.

The fall and possible elimination of private maternity services does not bode well for the state of maternity care generally. A 2025 Monash University study revealed that:

"Baby deaths were 53% higher, stillbirths were 56% higher and death soon after birth was 48% higher in multiprofessional public care versus obstetric-led continuity-of-private care".

- - Maternal and Neonatal Outcomes and Health System Costs in Standard Public Maternity Care Compared to Private Obstetric-Led Care: A Population-Level Matched Cohort Study, Professors Emily Callander and Helena Teede, Monash University, July 2025.

Not only is having your baby safer in private hospitals with a continuum of care for mums and bubs, it's also cheaper. Extract from the Monash University study:

"In these 368,292 matched pregnancies/births over four years to December 2019, the standard public model had an extra:

- 778 stillbirths or neonatal deaths (0.9 versus 0.4 per cent)

- 2,301 neonatal intensive care admissions (3.5 versus 1.3 per cent)

- 3,273 women with more severe vaginal tears (2.5 versus 0.7 per cent)

- 10,627 women with postpartum haemorrhage or excessive bleeding (9.6 versus 3.8 per cent)

- $5,929 cost per pregnancy ($28,645 versus $22,757) including costs to all payers when compared to the private obstetric-led model."

The overall additional cost of the standard public system is estimated at around $400 million annually, indicating potential for cost savings with private obstetric-led care.

- - Maternal and Neonatal Outcomes and Health System Costs in Standard Public Maternity Care Compared to Private Obstetric-Led Care: A Population-Level Matched Cohort Study, Professors Emily Callander and Helena Teede, Monash University, July 2025.

The shutdown of private maternity wards could see taxpayers up for, at least, an extra $1.7 billion a year to fill the breach.

- - Maternal and Neonatal Outcomes and Health System Costs in Standard Public Maternity Care Compared to Private Obstetric-Led Care: A Population-Level Matched Cohort Study, Professors Emily Callander and Helena Teede, Monash University, July 2025.

There are many factors that make maternity care challenging. Birth rates in Australia are at historic lows. Midwives are had to come by. Having paediatricians on-call 24/7 is expensive.

Another is health insurance companies only include maternity at the Gold level of cover. Despite holding Gold cover, often for years, mothers-to-be are shocked to discover they are not covered for an obstetrician, meaning they can be up for $10,000 in out-of-pocket costs.

Noone makes margin on maternity care. It has traditionally been cross-subsidised from other areas of the hospital because it's an important local service.

But over the last four years it has become increasingly untenable. The Australian Prudential Regulation Authority reports that health insurance companies have banked record profits of over $7 billion during that time. They also rake in $3.4 billion a year in 'management fees'.

Yet, over those four years they short-changed private hospitals by more than $4 billion on the treatments and care they provide. It can come as no surprise to anyone that this is unsustainable. If left unaddressed, more services, indeed, entire hospitals, will close.

So whether you have more babies to deliver or extra staff to deliver them, when you're being underpaid for the services you provide, then delivering 100, 1,000 or 10,000 babies each year doesn't help. In fact, you are just compounding the funding shortfall.

- - APHA summation of the issue.

Economy

In addition to being an indispensable part of Australia's health landscape, private hospitals are major drivers of economic activity and jobs...

Australia's private hospitals generated $24.128 billion last year in direct economic activity - an increase of $539 million on the previous year.

- - Australian Industry Data, Table 1 Key Data By Industry, Australian Bureau of Statistics 2023-24, May 2025.

However, the modest rise in income was outstripped by higher expenses over 2023-24 to $24.164 billion - up $921 million on the previous year.

- - Australian Industry Data, Table 1 Key Data By Industry, Australian Bureau of Statistics 2023-24, May 2025.

The gap between income and costs in 2023-24 (as stated above), saw the private hospitals record a sector-wide loss of -$34 million for the year.

- - Australian Industry Data, Table 1 Key Data By Industry, Australian Bureau of Statistics 2023-24, May 2025.

Private hospitals paid $12.55 billion in labor costs for staff in 2023-24, up $675 million on the year before, while only employing an additional 3,000 people on the previous year.

- - Australian Industry Data, Table 2 Labor Costs By Industry, Australian Bureau of Statistics 2023-24, May 2025.

In 2023-24 private hospitals employed 155,000 Australians - up 3,000 on the previous year - including nurses, allied health care professionals like radiographers and physiotherapists, as well as orderlies and administration staff.

- - Australian Industry Data, Table 1 Key Data By Industry, Australian Bureau of Statistics 2023-24, May 2025.

In 2023 Australian private hospitals employed 59,132 nurses - a 6.2% increase on the previous year. The state-by-state breakdown on nurses employed follows:

- - Private Hospital Nurses by State or Territory, Department of Health, Disability and Ageing, July 2025.

The Australian Government's Private Hospital Viability Health Check, released in November 2024, showed that almost one-third of private hospitals are operating at ongoing losses. Of the remainder, most are simply breaking even. Just a few are operating at a profit, but this is only at margins of 1-2%.

To put this is context, a research report by Ernst & Young in 2024 found that hospitals need a minimum 5% return in order to invest in the technologies, procedures and services expected of them. Further complicating this financial crisis, banks will not lend to hospitals when returns are below 10%.

- - Private Hospital Viability Health Check, Australian Government Department of Health and Ageing, November 2024.

Private Health Insurance

Let's be clear. There has always been argy-bargy between hospitals and health insurance companies, but what has emerged from the insurers over recent years is something not seen before - rapacious profiteering, gouging of insured people and record and growing short-changing of healthcare providers. The 12.7 million Aussies with private hospital cover are paying more and more to insurers, but getting less and less for it...

Since 2022 private health insurance companies in Australia have recorded unprecedented profits, a remarkable feat given annual premium increases have been historically low (3% on average or less each year up to 2025).

The after-tax profits of health insurance companies in Australia for the 12 months ending June 30 each year

- 2021-22 - $1.051 billion.*

- 2022-23 - $2.187 billion.**

- 2023-24 - $1.84 billion.***

- 2024-25 - $2.11 billion.****

- - *Quarterly private health insurance statistics June 2022 (released 24 August 2022) page 10,

- **Quarterly private health insurance statistics June 2023 (released 23 August 2022) page 10,

- ***Quarterly private health insurance performance statistics, Key metrics, September 2023 to June 2024 quarters (released 28 February 2025), Australian Prudential Regulation Authority.

- ****Quarterly private health insurance performance statistics, Key metrics, June 2024 to December 2025 quarters, Australian Prudential Regulation Authority.

On top of the record profits over recent years, the private health insurance industry increased its 'management fees' charged to customers in 2023-24 by a massive 18% - reaping another $3.4 billion a year from premiums.

- - Quarterly private health insurance performance statistics, Key metrics, September 2023 to June 2024, Australian Prudential Regulation Authority, August 2024.

In December 2024, the Commonwealth Ombudsman lifted the lid on phoenix policies. This loophole-exploiting practice sees health insurers scrap existing products, replace them with identical or near-identical services and sell them at much higher premiums.

At the time, Federal Health Minister Mark Butler publicly warned the insurers to stop the practice or he would legislate to block it.

But a CHOICE Magazine consumer investigation exposed that:

- On the same day the Minister announced average premium increases in February 2025 of 3.73%, HCF 'phoenixed' its Gold level cover.*

Extract:

[Minister] Butler called on health insurers to change their behaviour, threatening that if they didn't he would "consider legislative options to outlaw the practice into the future".

But on the same day Butler announced this year's annual premium increase, HCF brazenly phoenixed another Gold hospital policy.

While the health department published HCF's average fund increase of 4.95%, HCF closed its Premium Gold policy to new members and released an almost identical policy called 'Optimal Gold', with a 34.6% increase in price.

- Over the last four years cumulative average premium increases have been 11-12%. Under the phoenix policies over the same period premiums increased by 45%.**

Extract:

In fact, over the past four years, insurers have used this tactic to jack up the average price of Gold Hospital cover by 45%, while the "approved" average increase over the same period was 11.9%.

Given the health insurers' propensity to rip-off both ends of the spectrum – gouging their members at one end and short-changing hospitals at the other – we would welcome an ACCC investigation into these health insurance practices.

It is our view that they constitute unconscionable conduct, anti-competitive behaviour, represent abuses of market power and are, clearly, contrary to the interests of consumers of private health insurance.

- - *See the CHOICE article at: Insurers hiding soaring increases to top-level health cover, 13 May 2025.

- **See the CHOICE article at: Health insurance premiums to increase by 3.73% on 1 April, 27 February 2025.

While officially premiums went up an average 4.41% in April 2026, in reality, the majority of the 12.7 million Aussies with private hospital cover will pay much more.

Insurers with the lion's share of members are averaging 5.1% (Medibank), 4.8% (BUPA), 5.47% (NIB) and 4.96% (HCF)*. But, it gets worse. These are just the big-end-of-town's 'average' hikes. The insurance companies are jacking up their Gold policies by as much as 25%**.

- - *See Private Health Price Hikes List, via SBS News, 20 February 2026.

- **See Gold Health Insurance to Surge, via ABC News, 19 March 2026.

Out-of-pocket costs are a real concern for patients. There are no out-of-pocket costs for private hospitals, but there are for specialists, anesthetists and others.

Increasingly, private health insurers are selling more and more policies with exclusions and restrictions. These policies do not cover common procedures or only offer partial coverage, leading to high out-of-pocket costs.

While the number of people insured for hospital treatment has grown from 11.2 million in December 2019 to 12.7 million in December 2025, the number of people on exclusionary hospital policies has grown from 6.6 million to 8.9 million in the same period.

The percentage of policy-holders with exclusions built into their cover by insurers has grown by 18% in the last five years to a record 70.7%.

(If concerned about exclusions or restrictions in your health insurance policy, check out the Am I Adequately Covered? materials under the Publications section of this website.)

- - Quarterly private health insurance statistics December 2025, Spreadsheet Quarterly Private Health Insurance Membership and Benefits December 2025, Australian Prudential Regulation Authority, February 2026.

Prior to Covid, private hospitals received 90% of the premiums health insurers get each year. This funding ratio was considered the norm. However, over recent years the insurance companies have been keeping more for themselves while failing to meet the rising costs of healthcare delivery in hospitals.

Pass through of Patient Premiums to Patient Services

- - Australian Prudential Regulation Authority, Operations of Private Health Insurers Annual Report (FY20-23), Annual Private Health Insurance Performance Statistics (FY24 and FY 25).

When looking at the rising cost of providing healthcare each year and the funding provided by health insurers, the shortfall in meeting the actual costs of care is stark.

As the table below shows, the underpayment to private hospitals has grown and now consistently sits at over $1 billion a year - with a shortfall of $659.89 million (2022), $1.135 billion (2023), $1.254 billion (2024) and $1.12 billion in 2025.

- - Consumer Price Index, Australia, ABS (2025); APRA Quarterly Private Health Insurance Statistics, APRA (2025) (Note: Hospital-only benefits exclude nursing home type patients, medical, prostheses, total chronic disease management programs, and benefits paid for general treatment).

In addition to underpayments, the health insurance industry routinely engages in underhanded and unconscionable contract negotiation tactics, including:

- take-it or leave-it contract offers – refusing to negotiate in good faith, making one offer only and then using market power to influence other parties, such as doctors, to boycott hospitals that do not comply,

- playing hospitals against one another – using information from negotiations with other and competing hospitals to force positions on hospitals,

- the imbalance in information access – hospitals in a catchment area are disadvantaged when insurers are privy to the situation, practices and caseloads of competitors,

- bundling and inclusion of penalties for referrals – imposing restrictions on one hospital operator for the post-hospital care of patients and seeking to limit clinical decisions affecting patient rehabilitation. If patients require care nonetheless, the contracted hospital is penalised,

- payment schedules – these are notoriously missed and delays of many months are typical,

- contracting delays – contract renegotiations are being delayed by months and in some cases by more than a year, meaning hospitals cannot even try to get a better deal for the costs they incur,

- failure to contract at all – some health insurers that have had longstanding contracts with hospitals have simply refused to enter into new contracts, forcing those affected insured patients to pay significant out-of-pocket expenses or go to a different hospital,

- aggressive audits – these have gone beyond the remit of insurers' rights to patient information, with insurers insisting on a patient's full medical history, not just the procedure, treatment and services involved in the admission being claimed.

- Under so-called 'bundling', insurers restrict what care, especially rehabilitation, their members will receive before they even get sick or injured. Patients only become aware of this when it's too late and they are at their most vulnerable.

- The insurers have built exclusions into 70% of policyholders' cover, delivering their members less while exposing them to hefty and often hidden out-of-pocket costs.

- It has emerged, in writing, that insurers are now coercing doctors to force hospitals to provide treatments at less than cost or risk losing patients altogether, while also demanding they pre-approve what services hospitals can offer in the future or forgo payments.

- They flagrantly abuse paying legislated minimum fees per episode of care. Insurers insist that averaging the minimum payment across multiple episodes is enough. By definition, that means they are routinely paying hospitals below basic rates.

Light needs to be shed on these contracting tactics, with the APHA calling on the Federal Government for a Mandatory Code of Conduct to force transparency and accountability on these practises.

- - Examples provided to the APHA by member hospitals and reported to the Federal Government for action.

Given the abuses in the contracting regime, the Australian Competition and Consumer Commission (ACCC) has long held the view that a Code of Conduct with teeth is necessary to address the issues.

Extracts from the ACCC evidence at Senate Committees:

Report to the Australian Senate on anti-competitive and other practices by health funds and providers in relation to private health insurance for the period ending 30 June 2000

- The Commission is of the view that many of these issues could be addressed by the implementation of the Code of Practice for Hospital Purchaser Provider Agreement Negotiations between Private Hospitals and Private Health Insurers currently being developed by hospitals and health funds.

- There is no doubt that profitability in the private hospital sector has been reduced as a result of the contracting environment. However, this has had the effect of funds being able to offer no-gap policies for hospital accommodation services without the need for massive premium increases.

- The Commission would recommend that the Department of Health and Aged Care or an independent third party, acceptable to both hospitals and health funds, intervene in the process and mediate between the parties to ensure the code is quickly finalised.

- Given the level of animosity between the two sectors, it may be that stronger measures are required to make the sector function if the code cannot be agreed to or fails to remedy the problems. Again this is an area for the Department of Health and Aged Care to assess.

Report to the Australian Senate on anti-competitive and other practices by health funds and providers in relation to private health insurance for the periods 1 July 2000 to 31 December 2000 and 1 January 2001 to 30 June 2001

- The code provides a range of safeguards for all parties to contract negotiation and, as a consequence, also the consumer. Underlying the code is the principle that there is no requirement for either party to enter into a contract if the result does not reflect the needs and aspirations of the party or parties.

Report to the Australian Senate on anticompetitive and other practices by health funds and providers in relation to private health insurance for the period 1 July 2005 to 30 June 2006

- In the ACCC's view, confrontational contract negotiation processes might be better resolved through a reinvigorated code than by direct disputation.

Report to the Australian Senate on anti-competitive and other practices by health funds and providers in relation to private health insurance for the period 1 July 2006 to 30 June 2007

- The ACCC repeats its observation in the previous report that confrontational contract negotiation processes might be better resolved through a reinvigoration of the now apparently disused voluntary Code of Practice that was developed to help reduce disputes in contract negotiations.

- - Australian Government, Australian Competition and Consumer Commission (ACCC), Report to the Australian Senate on anti-competitive and other practices by health funds and providers in relation to private health insurance for the period ending 30 June 2000 < www.accc.gov.au/about-us/publications/serial-publications/private-health-insurance-reports/private-health-insurance-report-january-to-june-2000>;.

- Australian Government, Australian Competition and Consumer Commission (ACCC), Report to the Australian Senate on anti-competitive and other practices by health funds and providers in relation to private health insurance for the periods 1 July 2000 to 31 December 2000 and 1 January 2001 to 30 June 2001 < www.accc.gov.au/about-us/publications/serial-publications/private-health-insurance-reports/private-health-insurance-report-2000-01>;.

- Australian Government, Australian Competition and Consumer Commission (ACCC), Report to the Australian Senate on anticompetitive and other practices by health funds and providers in relation to private health insurance for the period 1 July 2005 to 30 June 2006 < www.accc.gov.au/about-us/publications/serial-publications/private-health-insurance-reports/private-health-insurance-report-2005-06>;.

- Australian Government, Australian Competition and Consumer Commission (ACCC), Report to the Australian Senate on anti-competitive and other practices by health funds and providers in relation to private health insurance For the period 1 July 2006 to 30 June 2007 < www.accc.gov.au/about-us/publications/serial-publications/private-health-insurance-reports/private-health-insurance-report-2006-07>;.

Vertical Integration

Vertical integration in healthcare has been a disaster in the US. Often referred to as US-style managed care, it sees health insurance companies owning/operating clinical services, including hospitals, to cut costs with quality care of patients the first casualty...

In 2023 a Harvard University-led study into the impact of vertical integration on 2.6 million patient visits across 5,488 physicians found that:

"Physicians significantly alter their care process (e.g. in using anaesthesia with deep sedation) after they vertically integrate, and there is a substantial increase in patients' post-procedure complications".

They also found "the financial incentive structure of the integrated practices is the main reason for the changes in physician behaviour because it discourages the integrated practices from allocating expensive resources to relatively unprofitable procedures", and concluded "that vertical integration negatively affects the quality of care".

- - The Impact of Vertical Integration on Physician Behavior and Healthcare Delivery: Evidence from Gastroenterology Practices, Soroush Saghafian et al, National Bureau of Economic Research, February 2023.

Research Extract:

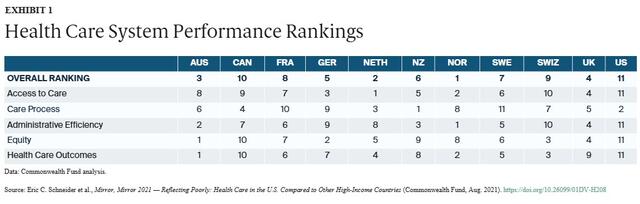

"Health care outcomes reported here refer to those health outcomes that are most likely to be responsive to health care. On this domain, Australia, Norway, and Switzerland rank at the top of our 11-nation group (Exhibit 1). Norway has the lowest infant mortality rate (two deaths per 1,000 live births), while Australia has the highest life expectancy after age 60 (25.6 years of additional life expectancy for those who survive to age 60)."

"The U.S. ranks last overall on the health care outcomes domain (Exhibit 1). On nine of the 10 component measures, U.S. performance is lowest among the countries (Appendix 8), including having the highest infant mortality rate (5.7 deaths per 1,000 live births) and lowest life expectancy at age 60 (23.1 years). The U.S. ranks last on the mortality measures included in this report, with the exception of 30-day in-hospital mortality following stroke. The U.S. rate of preventable mortality (177 deaths per 100,000 population) is more than double the best-performing country, Switzerland (83 deaths per 100,000)."

"The U.S. has exceptionally poor performance on two other health care outcome measures. Maternal mortality is one: the U.S. rate of 17.4 deaths per 100,000 live births is twice that of France, the country with the next-highest rate (7.6 deaths per 100,000 live births)."

"The second is the 10-year trend in avoidable mortality. As depicted in Exhibit 8, all countries reduced their rate of avoidable mortality over 10 years, but the U.S., with the highest level in 2007, reduced it by the least amount — 5 percent reduction in deaths per 100,000 population by 2017 — compared to 25 percent in Switzerland (by 2017) and 24 percent in Norway (by 2016)."

- - Mirror, Mirror 2021: Reflecting Poorly - Health Care in the U.S. Compared to Other High-Income Countries, Eric C. Schneider et al, The Commonwealth Fund, August 2021.

An investigation into a new wave of health care consolidation where health insurance and retail conglomerates are rapidly acquiring providers, from primary care practices and surgery centers to home-based and post-acute care, found the following:

"With dominant market power, the new health care conglomerates can dictate which physicians patients can see, which medications are prescribed to them, and which insurance plans they enroll in."

"By acquiring medical practices, these corporate employers can shorten visit times, require more clinical coding and box-checking, and replace physicians with lower-cost clinicians."

"Meanwhile, by coordinating across lines of business, conglomerates like UnitedHealth can squeeze out independent practices and community pharmacies."

"They can also shuffle money between subsidiaries and use other financial tactics to skirt regulations and exploit payment loopholes, increasing health care costs."

"Vertical consolidation also enables patient steering: conglomerates can push patients to receive care at their own provider subsidiaries."

"In doing so, these companies squeeze out local providers, such as independent physician practices and community pharmacies."

"Steering also generates "captive revenue", which allows conglomerates to game federal regulations requiring that government payments are spent on patients, not profits."

"Further, these conglomerates use their insurance-side subsidiaries to pressure independent practices to sell to their provider-side subsidiaries, effectively "flipping" new patients to their own medical practices and insurance plans."

"In addition to increasing overall enrollment, flipping gives conglomerates a tool to drive "favorable selection", or the practice of enrolling patients who are systemically profitable, even after risk-adjustment."

- - Medicare Advantage and Vertical Consolidation in Health Care, American Economic Liberties Project, Rooke-Ley, Hayden, April 2024.

Extracts from US House of Representatives, Committee on Ways and Means:

1. Consolidation in any industry raises concerns about reducing competition, because without competition, prices go up, incentives to innovate are reduced, and quality goes down, reducing value for consumers.

2. Beyond insurer-to-insurer horizontal consolidation, insurers over the past decade have been vertically integrating with providers, including hospitals, physician practices, nursing homes, home health agencies, pharmacies, and ASCs. This form of integration between insurers and providers raises concerns of price increases and access barriers for patients covered by rival insurers.

3. Over the past decade, insurers have been shifting away from solely providing insurance to reinventing themselves as health care delivery organizations.

4. This transformation has been spurred by several factors, including periodic threats of a single-payer health system putting private insurers out of business; the ongoing shift to value-based payments, which require the ability to manage financial risk and coordinate care delivery across the continuum of care; and competition from fully integrated, full-risk population-health delivery systems, which have achieved high levels of quality performance in both the commercial insurance market and Medicare Advantage, allowing these integrated delivery systems to gain market share and substantial quality bonuses under value-based payment arrangements.

5. However, the major reason why insurers are vertically integrating with providers of all types of care delivery is to control more of the production of health care and, in turn, capture the revenues created along the production path.

6. Proponents of vertical integration have argued that integration will lead to benefits, including increased efficiencies through the lowering of administrative costs through economies of scale; the ability to devote more resources to improving care delivery infrastructure, such as clinical care redesign, more quality-improvement staff, investment in interoperable health information technology capabilities to improve communication, and investment in enhanced analytics; and improved clinical integration and coordination of care across providers within a health system, resulting in improved quality of care and better patient outcomes.

7. Instead, vertical integration leads to increased spending due to shifts from lower-cost to higher-cost treatment settings and due to increases in payment rates to providers because of increased negotiating power. Increases in payment rates can translate to higher premiums paid. Quality does not improve.

8. In closing, health care consolidation is a major problem in the U.S. health system. It reduces competition and contributes to increased health care spending. It also has not yielded improvements in quality or health outcomes for patients. When hospitals and doctors face less competition, they charge higher prices without improvements in quality.

9. This is also true for insurers, which charge higher premiums when faced with less competition. Lack of competition stifles innovation that could reduce spending or improve patient outcomes. Competition creates incentives to have both lower prices and higher quality; consolidation removes the quality-improvement incentive and, thus, leads to worse outcome.

- - Health Care Consolidation: The Changing Landscape of the U.S. Health Care System, US House of Representatives, Committee on Ways and Means, Testimony, Health Care Consolidation, 17 May 2023.

Research Extract:

"Vertical consolidations among health care firms can lead to lower prices if they generate efficiencies (cost savings) and encourage more aggressive competition among firms in the market."

"In other situations, however, vertical consolidations can lead to higher prices by facilitating the exercise of monopoly power."

"When health care firms consolidate vertically, individual competitors—physician organizations, hospitals, or insurers—are often hurt (for example, individual competitors may lose customers or even be driven out of business)."

"Exclusive dealing contracts are often thought of as integration through contract rather than through ownership. Their competitive impact may be quite similar to vertical integration because under exclusive dealing contracts at least one of the parties in the exchange agrees to trade only with the other."

"In general, the case of insurery merging, forming a joint venture, or signing an exclusive contract with providery specifying that providery will treat only those patients insured by insurery (thereby foreclosing other insurers' access to provider y) has the potential to be anticompetitive, specifically to decrease competition in the market for health care financing and thus to allow insurer Y to exercise market power under certain conditions."

- - The Effects of Vertical Consolidation in Health Care Markets, Managed Care and Monopoly Power, Wilson, Haas, Smith College.

Research Extract:

"Hospitals and insurers interact in a vertical market. Downstream insurers sell plans to consumers, offering access to upstream hospitals. VI between these players has theoretically ambiguous welfare effects."

"On the positive side, VI aligns insurer and hospital incentives to eliminate double marginalization and limit wasteful spending."

"On the negative side, it grants market power to integrated firms, creates incentives for VI hospitals to increase rival insurers' costs or foreclose their access, and for VI insurers to limit patient access to rival hospitals."

"We focus our analysis on inpatient care provided by general acute care hospitals in Santiago. This is the largest healthcare market in the country, accounting for more than one-third of private hospitals and around one-half of the capacity."

"Inpatient care accounts for most medical spending and comprises fewer players, exacerbating the strategic concerns associated with VI. We limit our attention to the 11 leading private hospitals, which receive 74 percent of admissions in the market, the remainder captured by a large set of small hospitals."

"Enrollees switching to a VI insurer experience a change in plan coverage across hospitals."

"Switchers face 3 percentage points higher coverage at hospitals integrated with their new insurer and 4 percentage points lower coverage at rival hospitals. Likely as a result of the appeal of higher coverage, switchers are more likely to choose hospitals integrated with their insurer."

"Insurers respond to a VI ban by drastically changing their plan supply. The coverage for hospitals in the base coverage tier falls substantially at both VI and non-VI insurers by 6.5 and 21.8 points, respectively. In contrast, the coverage in the preferential tier increases slightly for both. The combination of these changes leads to a larger gap in generosity across tiers, intensifying demand steering through provider networks."

"The average price of VI hospitals to their formerly VI insurers increases by 23.2 percent, consistent with higher hospital markups and double marginalization. VI insurers increase premiums by 9 percent due to higher costs and the elimination of the incentive to attract enrollees with lower premiums to steer them toward their integrated hospitals."

"In the hospital market, VI hospitals lose almost half their market share as former partners no longer steer demand their way."

- - Vertical Integration and Plan Design in Healthcare Markets, Jose Cuesta, Carlos Noton, and Benjamin Vatter, Chile, May 2025.

Article Extract:

"With vertical integration we find that a breakdown of a contract will always occur. There may be two reasons for not concluding a contract. First, hospitals may choose to soften competition by contracting only one insurer in the market. Second, insurers and hospitals may choose to increase product differentiation by contracting asymmetric hospital networks. Both types raise total industry profits and lower consumer welfare."

"We find that the most profitable exclusive contract of a hospital-insurer pair is a contract that prevents the access of the competing insurer to their hospital. This raises profits for the hospital-insurer pair because the competing insurer becomes less attractive for consumers."

"We obtain a similar exclusive strategy if the hospital-insurer pair vertically integrates. Another exclusive strategy of a vertically integrated hospital-insurer pair is to prevent the access of their own enrollees to the competing hospital. This strategy introduces asymmetry on the insurance market which raises total industry profits. Furthermore, this strategy reduces the outside option of the competing hospital, thereby weakening its bargaining power."

- - Vertical integration and exclusive vertical restraints between insurers and hospitals, Rudy Douven et al, CBP Netherlands Bureau for Economic Policy Analysis, March 2010.

In 2023 an Australian Medical Association report warned that Australia could be heading towards a US-style managed care health system if health insurance companies continue their push for vertical integration.

It said about 40% of patients are missing out on access to out of hospital services, in large part because the funding models don't support the innovation we know exists in the private hospital sector.

It also highlighted the danger that vertical integration is leading to outcomes that are not in patients' best interests.

- - Out-of-hospital models of care in the private health system, AMA, October 2023.